YTD means Year Till Date.

YTD return is how much profit (or loss) an investment makes from the last financial day of the previous year. The last financial day varies from one institution to the next. However, YTD is mostly used to reference the period of time between 31st Dec of the previous year and your current date (today).

While you’ve enjoyed a couple of breaks this year, the Aggressive Funds on Cowrywise haven’t. This is because the year till date (YTD) returns have been color green lately. ?

In fact, these investments have been working overtime as Nigerian stocks have gained 25% in just 5 months in 2022! In spite of inflation and all that’s currently happening in Nigeria, many Nigerian companies on the stock exchange have been reporting impressive profits, causing their values to skyrocket! If you held units of an aggressive fund, your YTD returns will have grown massively. This is because these funds contain majorly stocks.

Unlike conservative funds where returns are quoted on an annualised basis e.g. 10% P.A., returns on moderate and aggressive funds are calculated based on the YTD return.

YTDs help to calculate how a portfolio performs in relation to recent times.

Let’s break it down

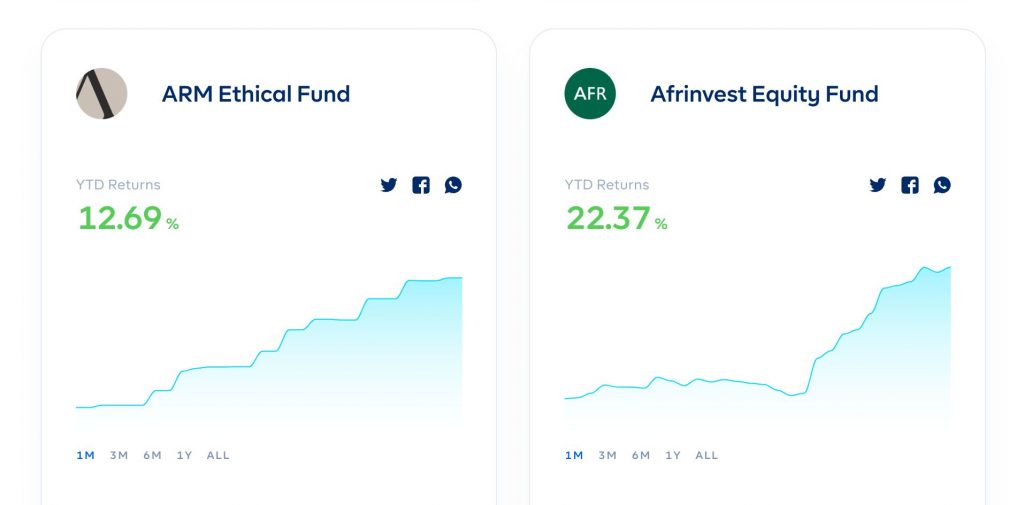

Let’s say you invested in either Meristem Equity Market Fund or Afrinvest Equity Fund on the 31st of December 2021 at NGN200, and today (May 20th 2022) these funds are now at NGN240 per unit. This means that your YTD return since December 31st is 20%. If you had invested say a total of N1M in both funds, you will now have N1M + N200,000 in returns.

If these funds continue to increase in price, your YTD return will increase. However, if they decline in price, your YTD return will decrease as well.

Comparing YTD Return to Per Annum Returns

As previously mentioned, returns earned on Conservative Funds (low-risk instruments) are quoted on an annualised basis. While returns earned on Moderate and Aggressive Funds are calculated based on the Year Till Date performance.

For context, Moderate and Aggressive Funds have a higher allocation to stocks and a small allocation to bonds and treasury bills. While Conservative Funds have a higher allocation to low-risk assets like bonds and treasury bills.

The major difference between YTD returns and Per Annum returns is that YTD returns show how the market has performed in the past (from today looking backwards). Also, they are used for securities like stocks and bonds that have prices that change every day. While Per Annum is used for short-term investments (e.g treasury bills, money market) that have a specific yield quoted on an annual basis. Here, the returns quoted per annum do not change.

Take advantage of the steady growth of Aggressive Funds on Cowrywise ?

Now that you know the differences between how each fund earns returns, it is also important to know this – Our listed aggressive funds have been growing rapidly!

Currently, the highest YTD return on Aggressive funds is at 22.37% and we’re not even halfway into the year yet!

However, it is also important to note that the investors who really eat good are those who invest for the long term. It is best to invest and watch your funds grow over a period of time than to expect a get-rich-quick scheme. As the name implies, Aggressive Funds are called that because they can be “aggressive” in terms of their gains and losses.

That’s why it is important to first understand your risk appetite. After that, you can be adequately guided on what percentage of your portfolio to put in aggressive funds.

Don’t sleep on this

Are you looking for funds that will work overtime for you? Then head over to the Cowrywise app and invest in the Aggressive fund of your choice now. ?

Click the image below to get started.

Timely update!

Kudos to the cowrywise team.